If you work in Korea, you will eventually hear the term “Year-End Tax Settlement” (연말정산). For many foreigners, it sounds complicated — but in reality, it’s a structured process that happens once a year and is largely handled online.

This guide explains what year-end tax settlement is, when and how to do it, and the special rules and benefits foreign employees should know.

1. What is Year-End Tax Settlement in Korea?

Year-end tax settlement is the process of reconciling the income tax you already paid throughout the year with the tax you actually owe.

In Korea, employers withhold income tax from your salary every month. At the beginning of the following year, the tax office recalculates:

- your total annual income

- applicable deductions or tax benefits

- the final tax amount

If you paid too much, you get a refund.

If you paid too little, you pay the difference.

For most employees, this happens once a year, through their employer.

2. When does it happen?

For income earned in 2025, the year-end tax settlement takes place in January–February 2026.

Typical timeline:

- Mid-January: Hometax “Simplified Service” opens

- January–February: Employees submit data to their company

- By March 10: Final withholding tax return deadline (handled by employer)

3. How do you do it? (Hometax)

Most foreign employees use Hometax, the National Tax Service’s online platform.

The general flow is:

- Log in to Hometax

- Check your income and deductions via the Simplified Service

- Submit documents or consent forms

- Your company finalizes the calculation and files the return

Some companies download employees’ data in bulk (with your consent). Others ask you to download and submit the documents yourself.

4. Are foreign employees treated the same as Koreans?

It depends on your tax residency status.

If you are a Korean tax resident

You are treated the same as Korean employees for calculation methods.

You are considered a resident if:

- you have an address in Korea, or

- you stayed in Korea 183 days or more in the year

However, some deductions and special tax rules differ, which is where foreign employees need to pay close attention.

5. New and important benefits for foreign employees

(1) Housing savings deduction now available

From 2025, foreign employees can claim a housing savings deduction (for example, housing subscription savings) if they are the spouse of a non-home-owning household head.

Previously, foreigners were excluded because they could not be registered as household heads. This rule has now been expanded.

Conditions:

- Total annual salary: 70 million KRW or less

- Tax resident in Korea

- Spouse of a non-home-owning household head

Deduction:

- 40% of the amount paid

- Up to 3 million KRW per year

This is a major change for married foreign workers living in Korea.

(2) Tax reduction for foreign technical professionals

Foreign employees with specialized qualifications may receive income tax reductions for up to 10 years.

You may qualify if you:

- provide technology under an engineering or technology-transfer agreement, or

- hold a bachelor’s degree or higher in science/engineering with overseas R&D experience

Benefit:

- 50% income tax reduction for up to 10 years

If you work for a designated strategic or specialized company (for materials, parts, or equipment industries), the reduction can be:

- 70% for the first 3 years

Highly skilled foreign talent under Korea’s advanced industry talent programs may also apply tax reductions to income received after February 28, 2025.

(3) Optional 19% flat tax for foreign employees

Foreign employees can choose between:

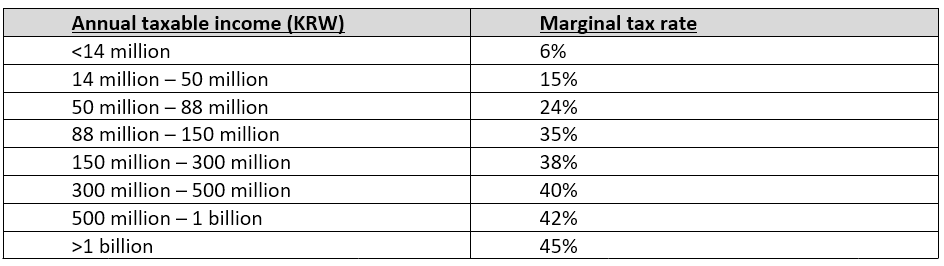

- the progressive tax rates (6%–45%), or

- a flat tax rate of 19%, for up to 20 years from their first working year in Korea

Important points:

- You must choose one — you cannot mix them

- If you choose the flat tax, no deductions or tax credits apply

- Not available if you work for a company in which you own 30% or more shares

This option can be attractive for high-income earners who do not rely on deductions.

(4) Income tax exemption for foreign language teachers

Some foreign teachers may be fully exempt from income tax under tax treaties.

If:

- Korea has a tax treaty with your home country, and

- the treaty includes a teacher or professor exemption clause,

then income from teaching or research may be exempt for a certain period.

Treaty rules vary by country, so this must be checked individually.

6. What if you are a non-resident?

Even if you are not a Korean tax resident, you must still settle Korean-source employment income.

However:

- Most deductions are not available

- Family-related deductions and special credits usually do not apply

In these cases, settlement is simpler but less favorable.

7. Practical tips for foreign employees

- Do not assume your company will automatically choose the best tax option for you

- Compare flat tax vs. progressive tax carefully

- Check whether you qualify for technical expert reductions

- Married employees should review housing deductions starting this year

- Keep records, even if you use the Simplified Service

The National Tax Service also provides:

- English guides on its website (National Tax Service – English)

- Multilingual manuals (English, Chinese, Vietnamese)

- English hotline: 1588-0560

Final thoughts

Year-end tax settlement in Korea is not just a formality — it’s a chance to recover overpaid taxes or reduce your tax burden, especially if you are a foreign employee with special eligibility.

The key is understanding which rules apply to you and making informed choices — particularly when it comes to flat tax options and special reductions.

Leave a Reply